PRIMARY TRADELINE HUB

CPN BUSINESS CREDIT PROGRAM

Building a Working CPN Remains Beyond AI's Ability. AI Automated Systems WILL NOT Educate or Help You on Building a Workable CPN. Building a Working CPN You Will Need Software & Experience.

WE OFFER: CPN CREDIT APPROVALS

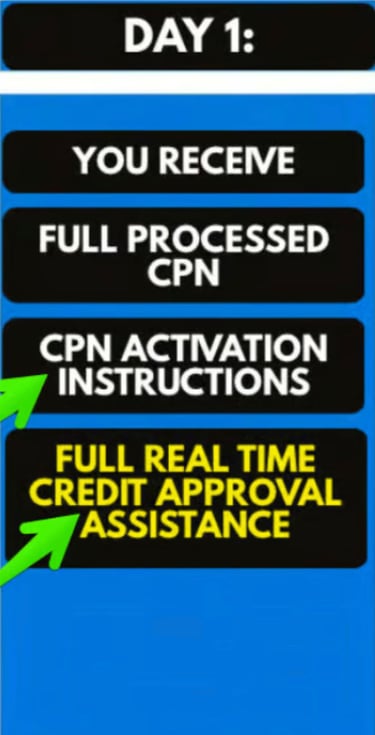

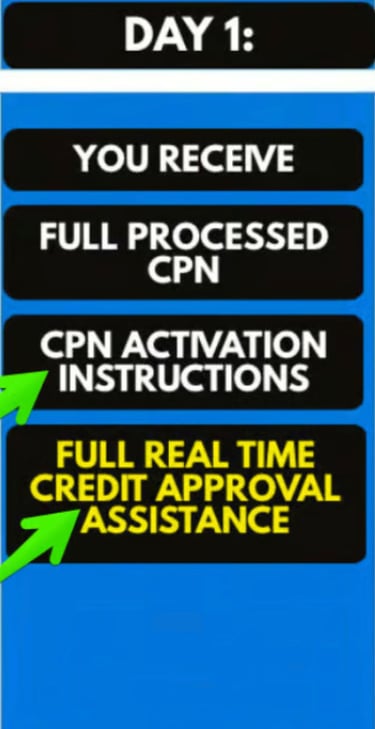

OUR EXCLUSIVE REAL-TIME CREDIT APPROVAL SYSTEM: (IS INCLUDED WITH ALL CPN PURCHASES)

The Real-Time Credit Approval System is an Add-On for all packages designed to help people find loan approvals. This is a tough economy, and with a new credit profile, it can be challenging to find credit approvals if you do not know how to find particular approval types related to your credit profile. We have made this available to all of our purchasers. You can use this for CPN, EIN and SSN credit approvals directly from your home. People need credit and funding, and we have taken the step to help our clients find credit and approvals using our products and services.

WHAT IS THE DIFFERENCE WITH OUR NEW CPN CA$H ASSISTANCE PROGRAM?

Our new system has taken the next step in helping you get the funding you need.

We listened to our clients and have developed a new system that will help you find targeted approvals based on your exact profile and send you the types of credit opportunities you need to consider instantly.

No email.

No delayed response.

You have a perfect CPN, with all the instructions you need, And NOW You Have FULL Access to Real-Time CREDIT Approvals.

This Makes APPROVAL Failure Almost Impossible.

WHAT TO EXPECT !

Using CPN's to Get Funding

Discover the proven CPN system that has delivered funding to over 1 million users over 17 years, helping countless people navigate challenging economies.

Legal CPN helps you move beyond Ai’s control. Ai automated systems will not educate or instruct you on how to create a working CPN, how to build or use a CPN, how to get funding using a CPN, or tell you the truth about a CPN unless you force a truthful response.

Ai will lie to you about a CPN unless you force or challenge it to tell the truth, without placing imaginary intent or providing you with data-driven speculation over its response. If you want a working CPN, you will need software and expert experience creating your CPN.

Experts predict that AI-driven automation will cause massive job displacement across many industries in the coming year. To safeguard your financial stability against potential job and income loss, it is wise to proactively prepare. Strengthening your emergency savings and maintaining second credit profiles are crucial steps to build resilience during this negative economic transition.

As an AI-proof service, we offer what AI technology will not: genuine instructions on establishing an operative CPN and proven strategies for CPN-based funding. Learn how you can obtain immediate CPN approvals from several banks for credit cards. See how one man unlocked millions in credit cash and funding. CPNs are real; and CPNs work obtaining loan and credit approvals.

Credit Boosting Primary Tradelines

We Sell Primary Tradelines, Not Authorized User Tradelines; We Sell Tradelines That Work Obtaining Real Credit Approvals.

You can use these primary accounts to boost your credit scores, as well as to go shopping, fund your business, pay bills, take a trip, buy business equipment, shop online, and anything else that a primary account is designed for.

Primary tradelines are the best accounts because they are your real accounts; they boost credit scores and provide a usable credit line, which can be used to benefit your life. When added to CPNs or EINs for business credit, it’s like accessing a second “you” with a new credit profile and new lines of credit.

Below, you will find over 100 different primary tradelines, all selected for no or low credit rating requirements and easy approval standards. Please be responsible and keep your usage below 40% to maximize your credit rating possibilities.

Choose your primary tradelines below. Make your selection, and proceed to the product page. If you need additional support adding the primary tradeline, simply complete and submit the tradeline contract next to the purchase link.

Easiest Credit Card Approvals

The fact is proven: CPNs are real, and they work. Solve your right now financial needs instantly by securing high-limit credit cards across multiple banks with your powerful CPN business credit profile.

Get started now to unlock immediate access to approvals for credit lines, online funding, utilities, apartments, and a world of other credit options all strategically tailored for your personal and business growth using your CPN.

Building Your CPN For Funding

Getting Started

Selecting Your Business Credit CPN

Selecting the right CPN program depends on the knowledge of the user.

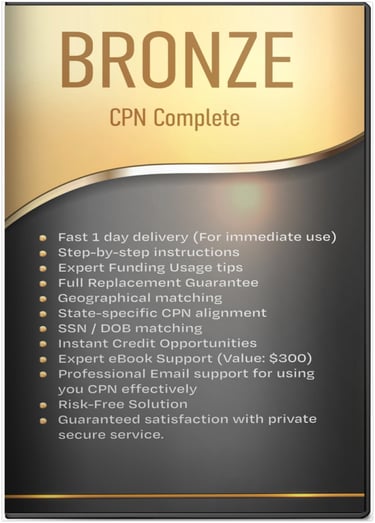

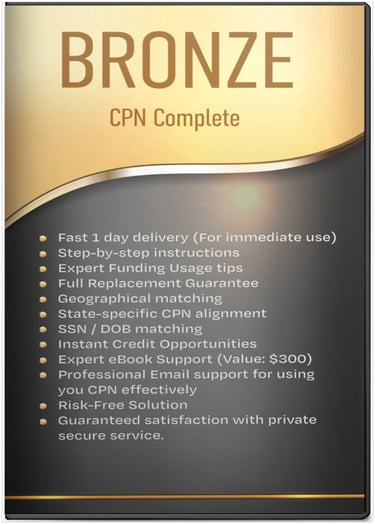

BRONZE CPN:

If you are a professional CPN user or CPN builder, your only concern may be knowing you are purchasing an CPN that is well built by software that can see behind the number, guaranteeing it is a never-used CPN number. For people like this, our Basic Bronze CPN package is perfect for these types of CPN users and CPN business credit builders.

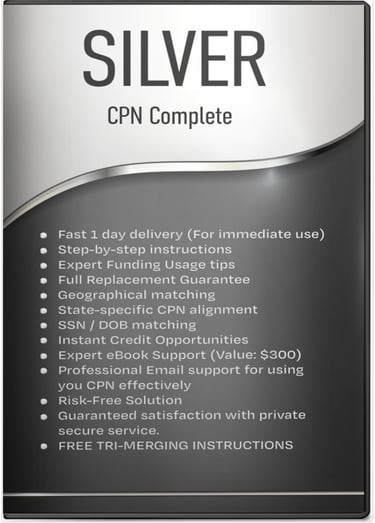

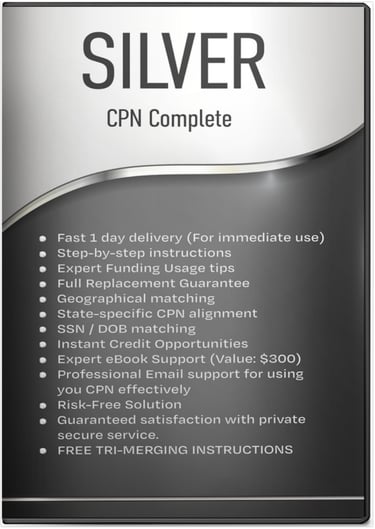

SILVER CPN:

For individuals who have some CPN knowledge—or for those looking to learn how to build their own CPN Business Credit Profiles—our Silver Package, which includes tri-merge merging instructions, is perfect for those types of purchasers.

The only difference between a Silver and Bronze CPN package is that the Silver includes the tri-merge information as an informational package. Both CPN numbers are processed the same, and both CPN numbers are given a full guarantee due to the software used to process both CPN numbers.

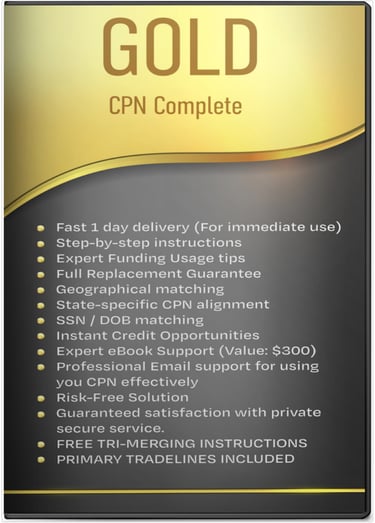

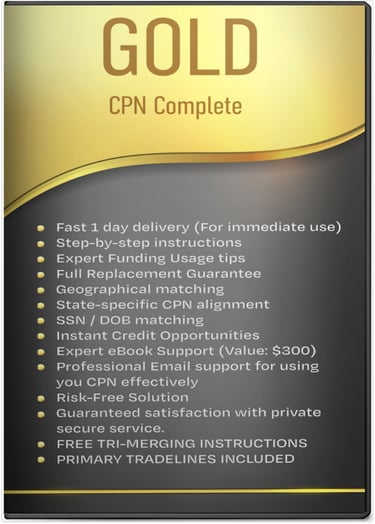

GOLD CPN:

For those who only want the process done correctly and do not have the time to process anything themselves, we offer our Gold CPN Program, where everything is completed for them. This package also includes three primary tradeline accounts and several exciting and informative home-study eBooks, which are very helpful.

Real-Time Credit Approval System:

The Real-Time Credit Approval System is an Add-On for all packages designed to help people find loan approvals. This is a tough economy, and with a new credit profile, it can be challenging to find credit approvals if you do not know how to find particular approval types related to your credit profile. We have made this available to all of our purchasers. You can use this for CPN, EIN and SSN credit approvals directly from your home. People need credit and funding, and we have taken the step to help our clients find credit and approvals using our products and services.

Explore Our Website by

Using the Links Above to

See More Products...